Scope 3 Materiality Assessment: Identifying relevant emission categories for CSRD reporting

Overview of Scope 3 materiality assessment

In Tanso, all Scope 3 categories are enabled by default. While the CSRD regulation strongly encourages reporting on every Scope 3 category, it allows you to exclude specific categories from your CCF if you provide valid reasoning. Common reasons for excluding certain Scope 3 categories include:

- Non-material emissions: Some Scope 3 categories may not be relevant to your organization because you have no associated activities. For instance, if your organizational structure does not include any franchises, Scope 3 Category 14 – Emissions from Franchises – would not apply to you.

- Challenges in data collection: Gathering the data required to calculate emissions in certain Scope 3 categories may be excessively difficult or time-consuming.

A materiality assessment is a method through which you can decide which Scope 3 categories are material to you and which are not. If a category is not material to you, through materiality assessment, you can clearly define your reasoning for the exclusion.

Tanso recommended Scope 3 categories

After going through reports from international organizations like Carbon Disclosure Project (CDP) and Science Based Targets Initiative (SBTi), we have created a list of Scope 3 categories which we think are material for the manufacturing sector. Additionally, Tanso is able to provide high-quality secondary data to account for emissions entailed in these categories in situations where primary data is not available or very difficult to gather. These categories are:

Categories for which a materiality assessment is required

Apart from the above recommended Scope 3 categories, there are 7 additional categories for which you would need to decide whether they are material to you or not. These categories are:

Decide which Scope 3 category is material for you by following the below mentioned decision trees. The decision trees include questions you should ask yourself and your stakeholders to decide on the materiality of the respective category, and examples on how to phrase your argument when deciding to exclude certain categories.

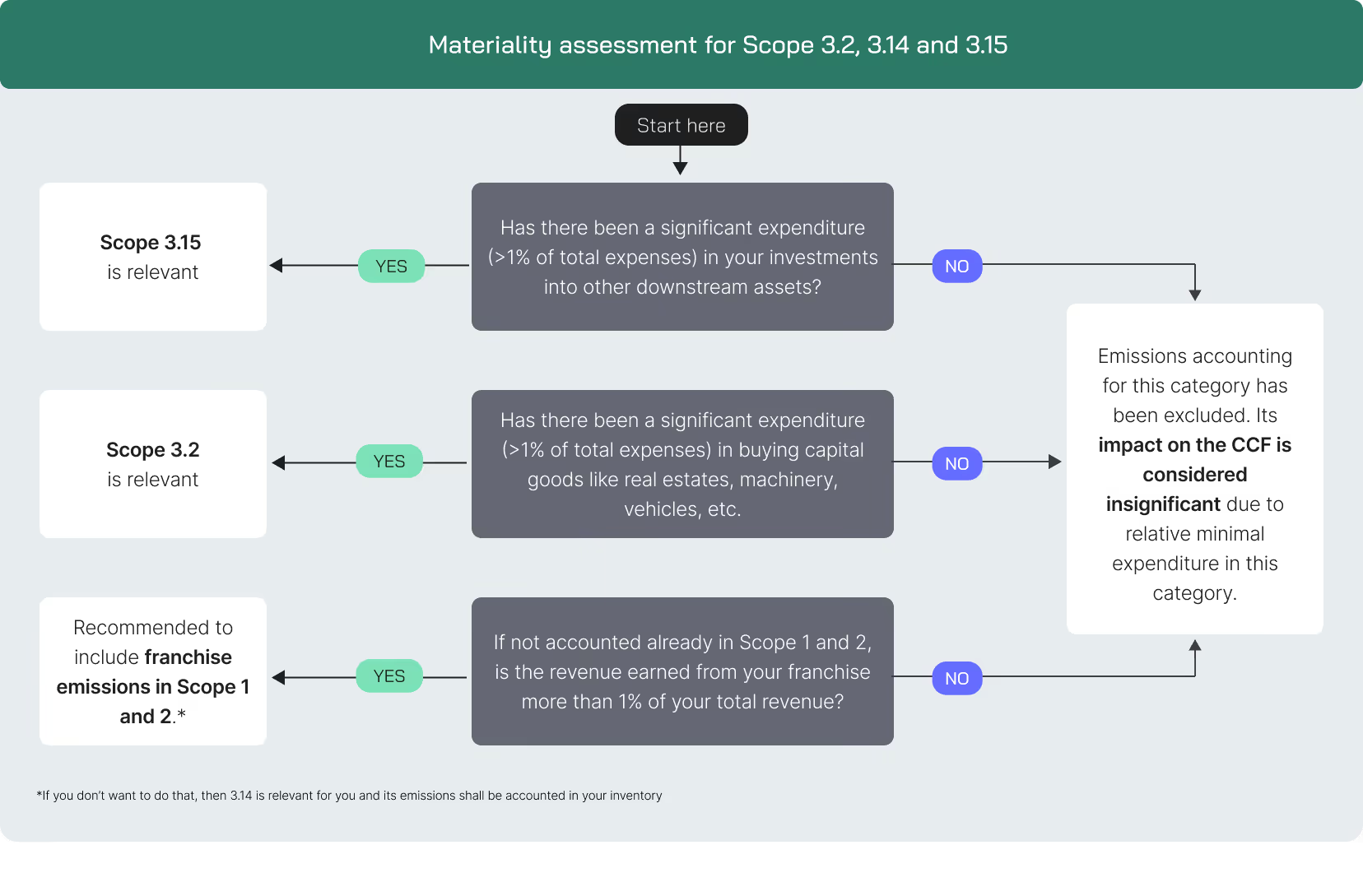

Scope 3.2, 3.14 and 3.15

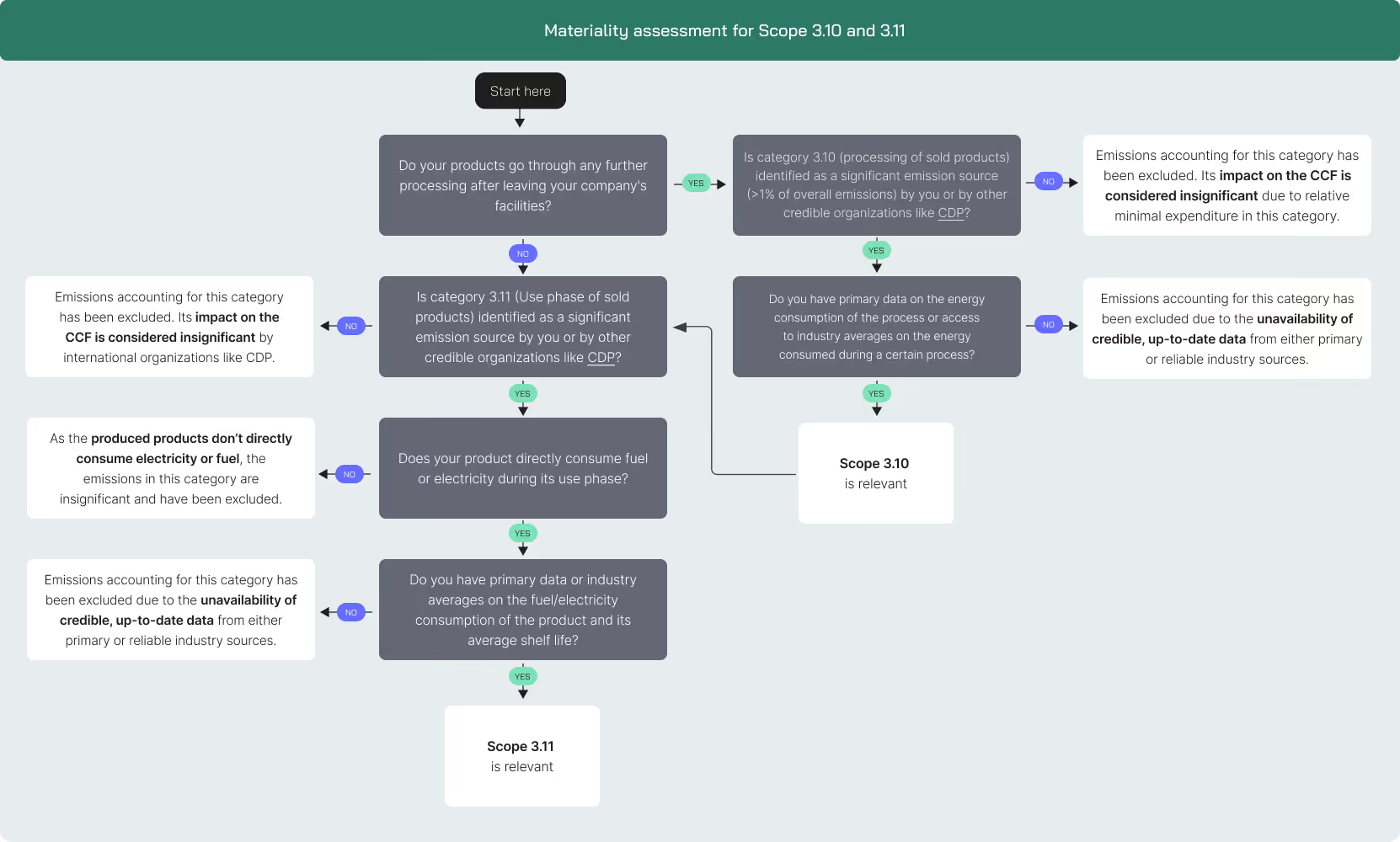

Scope 3.10 and 3.11

Accounting for categories 3.8 and 3.13

If you have complete operational or financial control over your upstream- and downstream-leased assets, you should account for their emissions in your Scope 1 and 2 inventory. This is in accordance with the GHG protocol CCF guidelines.

.avif)

.avif)

.jpg)