CSDDD and LkSG in comparison - similarities and differences between the EU supply chain laws

On April 24, 2024, the EU Parliament set a new standard in corporate responsibility by adopting the Corporate Sustainability Due Diligence Directive (CSDDD). On May 24, the EU Council also approved the CSDDD. This legislative measure aims to obligate companies to comprehensive due diligence in their supply chains, particularly regarding environmental and human rights standards. The CSDDD is not only a significant step for the EU but also a turning point compared to national laws such as the German Supply Chain Due Diligence Act (LkSG).

What is the German Supply Chain Due Diligence Act (LkSG)?

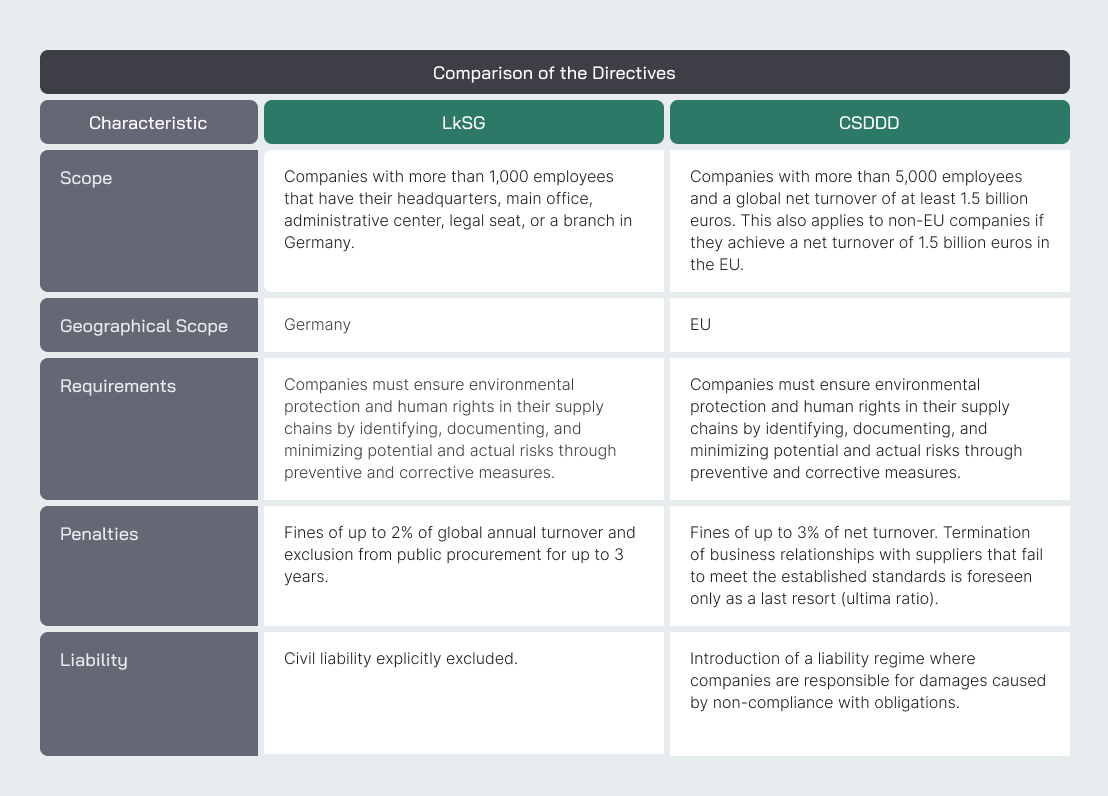

The German LkSG came into effect in 2023 and focuses on ensuring compliance with human rights and environmental standards along supply chains. It requires German companies with more than 1,000 employees to identify, document, and take measures to minimize risks to people and the environment. Violations can result in hefty fines and exclusion from public tenders.

What is the Corporate Sustainability Due Diligence Directive (CSDDD)?

The CSDDD obliges companies to systematically identify, prevent, and remediate environmental and human rights risks across their value chain. With the final adoption of the Omnibus I package by the Council of the European Union on 24 February 2026, however, the scope was significantly narrowed: going forward, only very large EU companies with more than 5,000 employees and a net turnover above 1.5 billion euros will be in scope. The originally planned lower thresholds (>3,000 and >1,000 employees) have been removed. Non-EU companies that exceed this turnover threshold in the EU market are also covered. Whether the thresholds will be lowered again at a later stage is to be reassessed under a review clause in 2029.

Timeline for Implementing the CSDDD

- By 26 July 2028: EU member states must transpose the CSDDD into national law (extended transposition deadline under Omnibus I).

- From 2029: First application of the national due diligence obligations for companies with more than 5,000 employees and a net turnover above 1.5 billion euros.

- 2029: Review clause — the European Commission will evaluate whether the thresholds should be adjusted and additional companies included.

Comparison of Sanctions

While the LkSG provides for fines of up to 2% of global annual turnover, the CSDDD — following the adjustments under Omnibus I — foresees fines of up to 3% of net turnover (originally 5%). An EU-wide harmonised civil liability rule was removed during the Omnibus I process; the design of civil liability is now left to the member states. The obligation to terminate business relationships in cases of severe and non-remediable adverse impacts has been softened: it now applies only as a last resort (ultima ratio), after other measures have been exhausted.

Comparison of LkSG and CSDDD

Key changes through the CSDDD

With Omnibus I, the original CSDDD was revised in several key areas:

- Risk-based due diligence: Companies are expected to prioritise risk assessments where the likelihood and severity of adverse impacts are highest — rather than carrying out a blanket deep-dive across the entire supply chain.

- Climate transition plans no longer part of the CSDDD: The obligation to draw up a climate transition plan has been removed from the CSDDD. For reporting companies, this obligation remains in place via the CSRD/ESRS (E1).

- No EU-wide harmonised civil liability: The originally planned EU-wide liability rule has been removed; the design is left to the member states.

- Termination of business relationships as ultima ratio: Business relationships must only be terminated when severe adverse impacts can neither be prevented nor remediated and milder measures have been exhausted.

- Reduced sanctions: The cap on fines has been lowered from 5% to 3% of net turnover.

- Review clause 2029: The European Commission will assess in 2029 whether the scope should be broadened and thresholds lowered.

Recommendations for Companies

To meet the new requirements, companies are well advised to invest in digitalisation and automation — particularly in corporate and product-level carbon accounting and in the structured collection of supplier data. Carbon accounting remains a central foundation of any sustainability strategy and continues to be mandatory for reporting companies under the CSRD (ESRS E1, including the Climate Transition Plan).

Furthermore, it is crucial to conduct a Double Materiality Assessment, which examines the financial, social, and economic risks and impacts of a company. This analysis is a central component of both the CSDDD and the Corporate Sustainability Reporting Directive (CSRD), whose requirements companies must also meet to remain compliant. These measures not only enable companies to fulfill regulatory requirements but also proactively take a leading role in sustainable corporate governance.

-

“According to the current draft bill from the Federal Ministry of Justice dated March 22, 2024, for the implementation of the CSRD, reporting companies will have the option to fulfill their reporting obligations under the Supply Chain Due Diligence Act (LkSG) through their sustainability report. This would enable the integration of reporting requirements and could help companies manage their compliance tasks more efficiently.”

.avif)

.avif)

.jpg)

-p-800.webp.avif)

-min-p-800.webp.avif)