FLAG Standard 2026: New Rules for Land Use, CO₂ Removals, and Emissions Accounting

Key summary

On 30 January 2026, the Greenhouse Gas Protocol published the Land Sector and Removals Standard. This document serves as a supplement to the existing Corporate Standard and Scope 3 Standard, establishing specific accounting and reporting requirements for companies involved in land management and carbon removal activities.

The Standard becomes effective on 01 January 2027. This summary outlines what can be expected of businesses that are required to comply, and how Tanso can help to enable FLAG conformity.

The main aim for the guidance is to harmonize emissions calculation methodology for all sectors which come under the FLAG sector:

- Forestry

- Agricultural goods

- Animal husbandry

- Food processors

- Beverage manufacturers

- Textile fiber producers

Under the current guidance, forestry has been excluded ❌

Key categories within the new standard

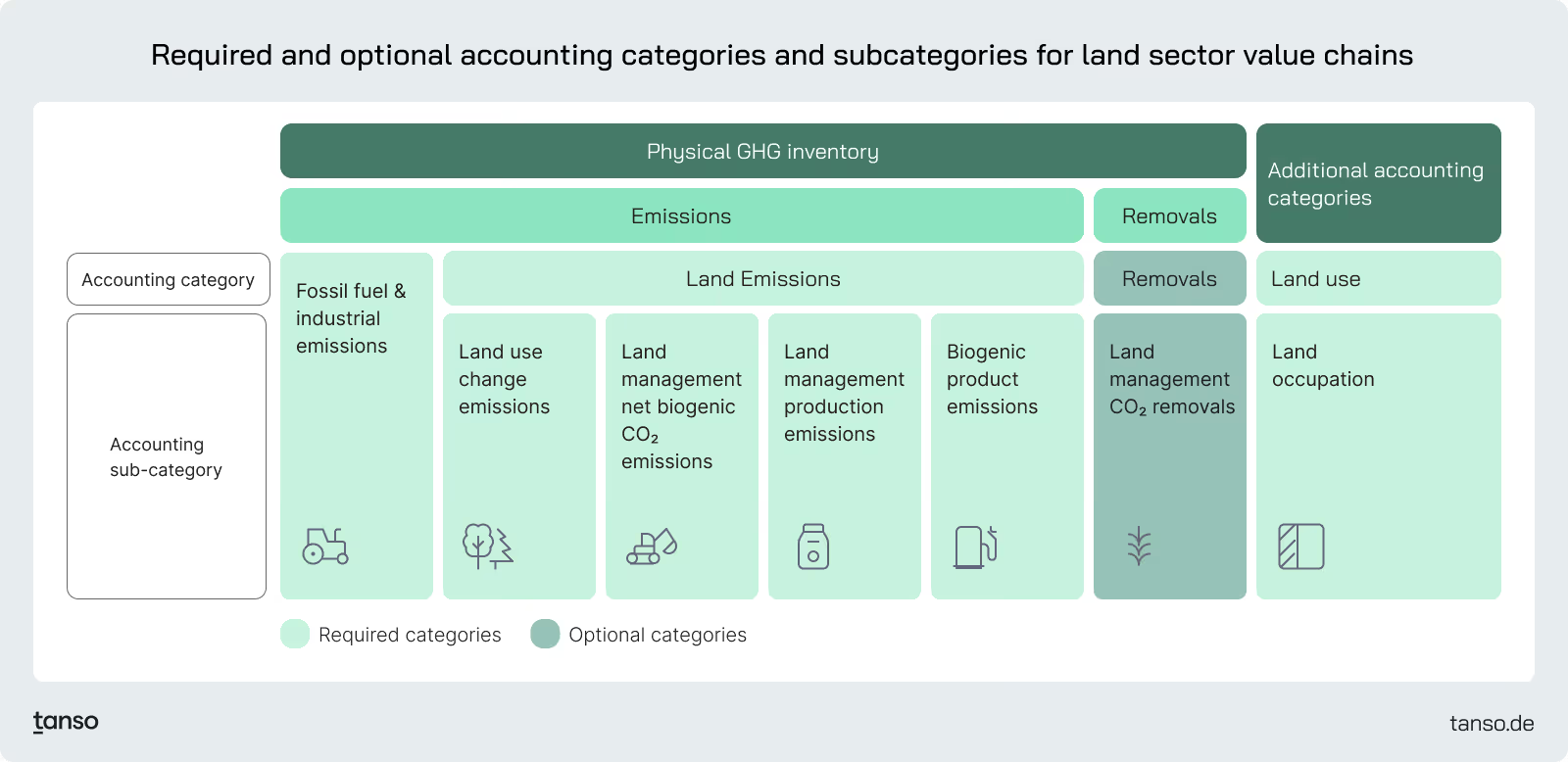

The Standard introduces specific accounting categories that companies must calculate to capture the climate impacts of land use. Key required categories include:

- Land Use Change (LUC): Emissions and removals resulting from the conversion of land between use categories, calculated over a 20-year period and including CO2, CH4, and N2O.

- Land Use & Leakage:

- Leakage: Emissions occurring outside a company’s boundary when land use changes or management decisions displace food or feed production, quantified using the Carbon Opportunity Cost (COC) approach.

- Land Use (Occupation): A physical metric measuring the land area occupied by FLAG commodities, reported in hectares and categorized by Scope 1 and Scope 3.

- Land Management: Ongoing emissions and removals on existing agricultural land, including:

- Net Biogenic CO2: Changes in carbon stocks driven by land management practices, accounted for using a stock-change approach.

- Production Emissions: Recurring agricultural emissions such as CH4, N2O, and non-biogenic CO2 from livestock, soils, and agricultural inputs.

- Biogenic product emissions: Biogenic product emissions arise from the oxidation of biogenic carbon, such as through biomass combustion or decomposition, and are reported separately as biogenic CO2.

Timeline

- Publication Date: 30 January 2026.

- Effective Date: 01 January 2027.

Companies impacted by these requirements should begin assessing their value chain traceability and data collection systems in preparation for the 2027 effective date.

Detailed Guidance: The six pillars of the LSR guidance

- Spatial boundary and Traceability

- Land use change emissions

- Land use and leakage

- Land management (CO2 and non-CO2)

- Removals

- Biogenic product emissions and removals

Spatial boundary and traceability

Spatial boundary defines the land areas whose emissions, removals, or other relevant metrics are included in an organization’s greenhouse gas inventory. These emissions fall under Scope 1 when the organization owns or controls the land, and under Scope 3 when the organization sources agricultural products from land it does not own or control. Establishing a spatial boundary enables accurate estimation of emissions or removals from the land where the agricultural products used by the reporting company are produced.

Traceability refers to the evidence or verification used to confirm the spatial boundary that an organization reports.

A company may define different types of spatial boundaries based on the level of detail and reliability of the information it has access to.

Providing physical traceability

When physical traceability is required, only specific chain of custody models are accepted under the LSR guidance. The book-and-claim approach is not permitted under LSR.

In addition, mass balance approaches are not allowed when input and output volumes are unknown, or when proportionality between inputs and outputs is not maintained (see P. 28 in the GHG Protocol Land Sector and Removals Standard).

Once spatial boundary and traceability are defined, companies can start calculating the emissions or removals of their produced or sourced raw materials. The LSR guidance breaks down emissions or removals from agricultural products into five categories.

1. Land use change (LUC)

Definition

Land use change emissions capture the GHG impacts that occur when land is converted from one category to another, such as:

- Forest → Cropland (negative impact)

- Barren land → Plantation (potential positive impact)

Land use change can result in either:

- Emissions (loss of carbon stock)

- Removals (gain of carbon stock)

Key requirements

- LUC accounting must include CO2, CH4, and N2O, and results must be reported in kgCO2e.

- Companies must calculate their net LUC emissions using one of the following approaches:

- Direct LUC (dLUC): used when the company has primary data and control over the land conversion.

- Statistical LUC (sLUC): uses commodity-level average land conversion factors when site-level data is unavailable.

Time horizon

LUC impacts must be assessed over a 20-year period.

Example:

If cocoa is produced in 2026, the reference year for land conversion assessment is 2006.

Allocation approach (discounting)

Once total LUC emissions are estimated, companies allocate emissions across the 20-year period using either:

- Linear discounting (default / preferred)Higher emissions are attributed closer to the conversion year, declining over time.

- Rationale: conversion emissions are front-loaded and decline as carbon pools stabilize.

- Equal discounting (alternative)Emissions are evenly distributed across 20 years.

- Companies must justify why equal discounting is more appropriate than linear discounting.

Special requirement for animal products

For livestock-related products, companies must include both:

- LUC impacts from grazing land

- LUC impacts from feed production land

2. Land Use and Leakage

Land use

Land use quantifies the area of land occupied by FLAG commodities.

- Expressed in hectares (ha)

- Categorized by scope:

- Scope 1: land owned/managed by the reporting company

- Scope 3: land used to produce purchased commodities

Land use is a physical metric, not an emissions metric.

Land leakage

Land leakage is applied when company actions indirectly reduce food production or divert agricultural production into non-food use, creating a demand for land elsewhere.

Leakage applies when companies

- Use agricultural products for non-food / non-feed purposes

- (e.g., biofuels, bio-based feedstocks)

- Permanently reduce food production through land conversion

- (e.g., cropland → forestland where removals are claimed)

- Reduce yields per hectare over the long term due to management changes

- (e.g., low-input farming causing yield decline)

Why leakage is included

The logic is that these actions may trigger:

- Increased agricultural expansion elsewhere

- Increased land conversion and emissions in other regions

How leakage is quantified

Leakage is quantified using the Carbon Opportunity Cost (COC) approach.

- Expressed in kgCO2e

- Represents additional carbon impacts occurring outside the reporting company’s boundary due to displaced production.

3. Land Management (LM)

Land management accounting covers ongoing emissions and removals that occur on existing agricultural land, driven by farming and livestock practices.

This pillar is split into two components:

3.1 Land Management - Net Biogenic CO2 Emissions

Definition

Net biogenic CO2 emissions represent the net change in carbon stocks caused by land management activities.

Examples of land management activities that can reduce carbon stocks include:

- Tillage and soil disturbance

- Overgrazing

- Loss of biomass and vegetation cover

These activities reduce soil organic carbon and biomass, releasing biogenic CO2 into the atmosphere.

Recommended accounting approach: Stock-change method

The guidance recommends a stock-change accounting approach, which compares carbon stock levels over time.

- If carbon stock decreases → net emissions

- If carbon stock increases → net removals

Regenerative agriculture practices can potentially increase carbon stocks.

Reporting methods

Companies can quantify LM biogenic CO2 emissions using:

Option 1: Primary data (preferred)

- Measure carbon stock change

- Convert carbon (C) to CO2 using 44/12

- Multiply by land area

Option 2: Secondary data

If primary carbon stock data is unavailable, companies may apply secondary emission factors, typically expressed as:

- kgCO2e per kg of agricultural product

- kgCO2e per hectare

3.2 Land Management - Production Emissions (Non-CO2 biogenic)

Definition

Production emissions capture recurring agricultural emissions including:

- Methane (CH4)

- Nitrous oxide (N2O)

- Non-biogenic CO2

Main emission sources include:

- Livestock emissions:

- Enteric fermentation

- Manure management

- Soil emissions:

- N2O emissions from nitrogen fertilizer application

- CO2 emissions from liming and urea application

These emissions are reported as part of land management because they are directly linked to agricultural production processes.

4. Biogenic Product Emissions

Biogenic product emissions refer to emissions released at the point of oxidation of biogenic carbon.

Example:

- combustion of bio-based fuels

- decomposition of biomass

These emissions are reported as biogenic CO2, and are treated separately from fossil CO2.

How Tanso supports

Tanso supports you in defining the spatial boundaries and traceability of your produced or purchased products. In addition, we help you develop the primary data required under the LSR guidance. Where primary data is not available, we provide reliable secondary data sources to calculate all FLAG-related parameters in your Corporate Carbon Footprint (CCF).

.avif)

.avif)

.jpg)

-p-800.webp.avif)

-min-p-800.webp.avif)