Sustainability reporting: An overview of the most important standards

In Europe, the manufacturing sector contributes a significant 22% of total greenhouse gas emissions. Industrial companies must therefore navigate their way through a maze of laws and standards in order to establish and improve suitable methods for carbon accounting.

Sustainability reporting plays a central role in this, as it creates transparency and enables companies to measure and communicate their environmental impact.

Frameworks such as the Corporate Sustainability Reporting Directive (CSRD) and the drafts of the International Sustainability Standards Board (ISSB) have significantly developed the landscape of sustainability reporting, improving the quality and consistency of reports. Nevertheless, choosing the right standard remains a challenge, as other guidelines exist alongside the CSRD and ISSB, and this article provides a summary of the most important standards.

Corporate Sustainability Reporting Directive (CSRD)

-

Mandatory for many European companies, detailed reporting.

Mandatory for many European companies, detailed reporting.

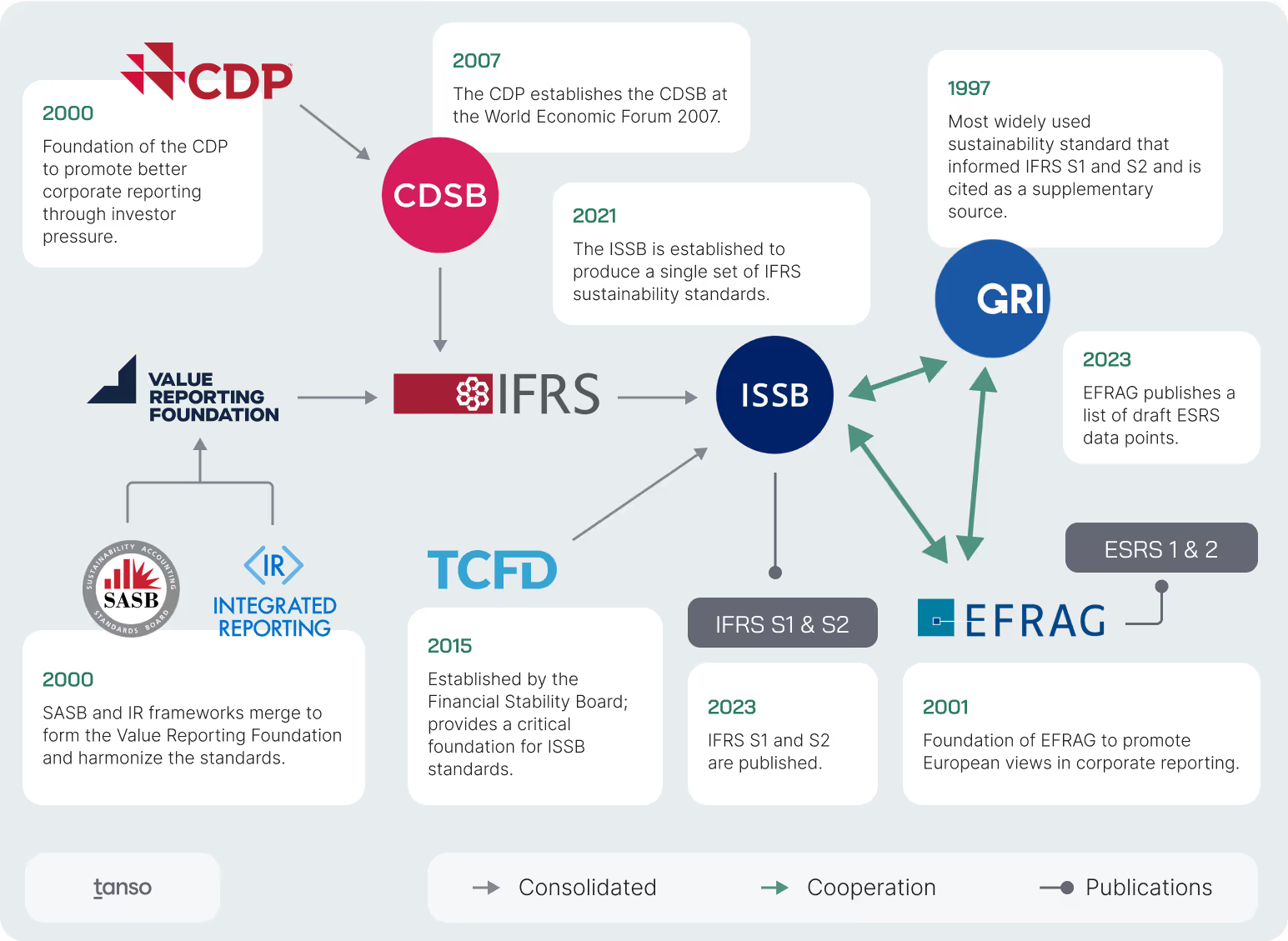

The Corporate Sustainability Reporting Directive (CSRD) came into force in January 2023 and extends the previous Non-Financial Reporting Directive (NFRD). It obliges around 50,000 companies in Europe to report on their environmental, social and governance (ESG) aspects. The CSRD requires relevant, comparable and reliable information on sustainability impacts and the associated risks and opportunities. It is enforced by the European Sustainability Reporting Standards (ESRS), which were developed by the European Financial Reporting Advisory Group (EFRAG).

International Sustainability Standards Board (ISSB)

-

Global harmonization, complementary to IFRS

Founded in 2021, the ISSB aims to develop global standards for the disclosure of sustainability information and to expand IFRS (International Financial Reporting Standards) to include non-financial disclosures. It works closely with the Global Reporting Initiative (GRI) and EFRAG. In 2023, the ISSB published two standards: IFRS S1 for general requirements and IFRS S2 for climate-related disclosures.

Global Reporting Initiative (GRI)

-

Internationally established, high effort

The GRI Standards enable organizations to report on the most significant impacts of their activities on the economy, environment and people, including human rights. Over 13,000 organizations in 90 countries use GRI for their sustainability reporting.

Deutscher Nachhaltigkeitskodex (DNK)

-

Germany-wide and across all industries

The German Sustainability Code (GSC) is a cross-industry transparency standard for reporting corporate sustainability performance and is available to companies of all sizes. Since 2017, the DNK has integrated the requirements of the NFRD.

Task Force on Climate-related Financial Disclosures (TCFD)

-

Climate-related financial information for financial markets

The TCFD, which was introduced in 2015, aims to create transparency with regard to the climate-related business activities of companies. It provides the financial markets with climate-related financial information to support well-founded capital allocation decisions.

Carbon Disclosure Project (CDP)

-

Used globally, evaluates environmental responsibility

The CDP is a global non-profit organization that offers companies, investors, regions, states, cities and authorities a platform for disclosing their environmental impact. Based on the data submitted, the CDP assesses the environmental responsibility of companies.

Greenhouse Gas Protokoll (GHG-Protokoll)

-

The gold standard for carbon accounting

The Greenhouse Gas Protocol is an internationally recognized standard for recording and reporting greenhouse gas emissions. It offers companies a comprehensive approach to quantifying and managing their emissions, divided into the categories Scope 1-3.

Non-Financial Reporting Directive (NFRD)

-

Predecessor to the CSRD

The NFRD, which was introduced in the EU in 2014, requires companies to publish a report on their ESG performance in addition to their annual management report. The aim is to assess the non-financial performance of large companies and promote a responsible business approach. The Corporate Sustainability Reporting Directive (CSRD) replaces the previous Non-Financial Reporting Directive (NFRD) and will be implemented in stages between 2025 and 2028.

Securities and Exchange Commission Rule (US SEC Rule)

-

Mandatory standardized climate reporting for listed companies in the USA

The US Securities and Exchange Commission (SEC) regulation introduced in 2022 requires listed companies to provide standardized climate reporting. From March 2024, companies must include climate-related disclosures in their annual reports and registration statements in order to provide investors with reliable information.

Reporting standards and their relationships to each other

.avif)

.avif)

.jpg)

-p-800.webp.avif)

-min-p-800.webp.avif)