CSRD Implementation Act: German government draft reflects Stop-the-Clock and new thresholds

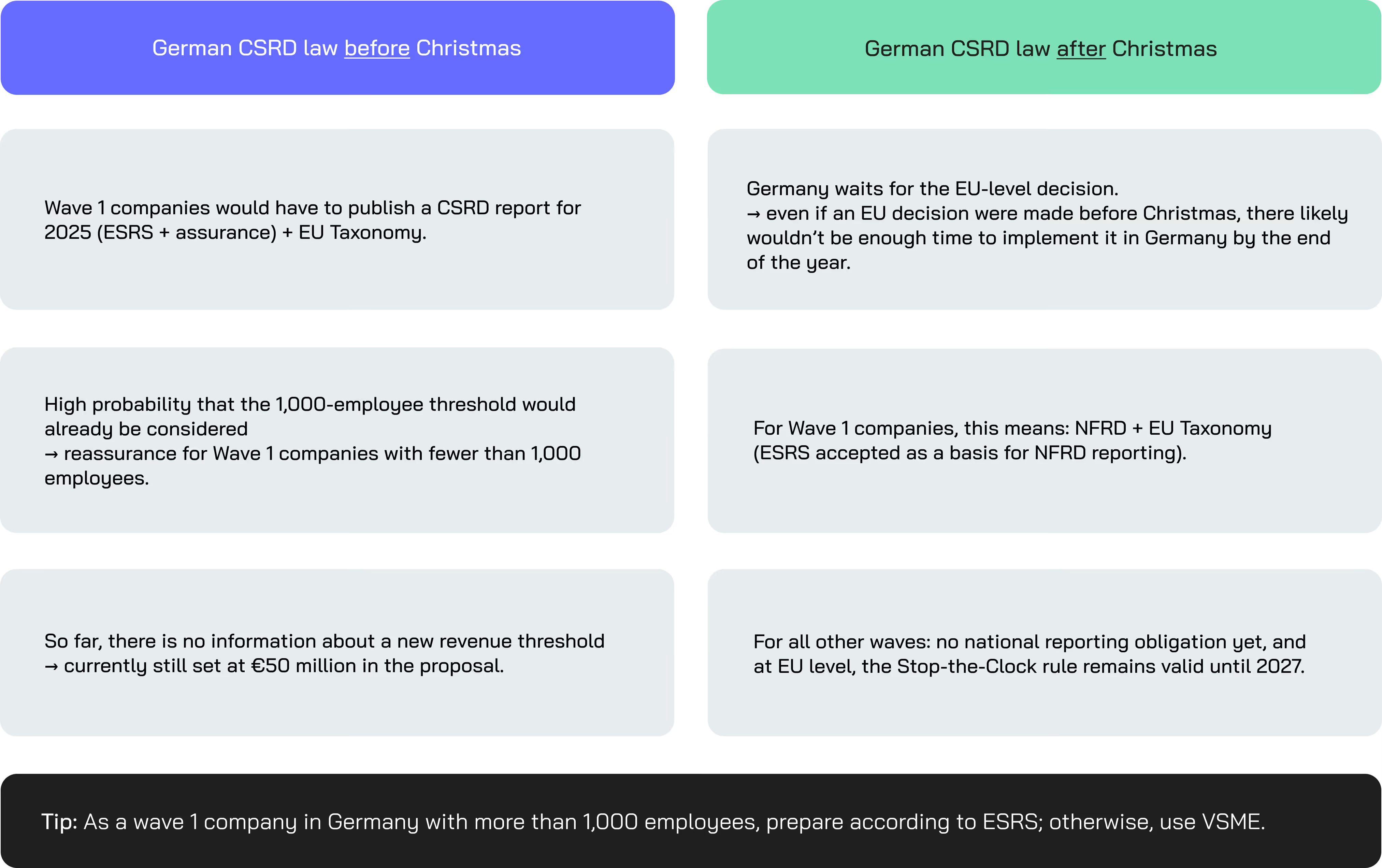

On October 9, the German government draft for the CSRD Implementation Act was referred for further consultation to the leading Committee on Legal Affairs and Consumer Protection, as well as to the Committee on Economic Affairs and Energy, the EU Committee, and the Budget Committee. The government draft already takes into account the Stop-the-Clock agreement and the 1,000-employee threshold proposed in the EU Omnibus procedure. Since Germany should have implemented the CSRD by June 2024, the European Commission has already initiated infringement proceedings against Germany. A quick agreement is therefore expected. It remains open whether a potential new revenue threshold will already be implemented during the national discussions. However, it is quite likely that the German law will await the final EU-level agreement to incorporate the new thresholds and avoid imposing unnecessary reporting obligations on companies.Until then, NFRD (including the EU Taxonomy) continues to apply in Germany for public-interest companies with more than 500 employees (Wave 1).

On October 17, the German Bundesrat also adopted its opinion on the draft law. While largely agreeing with the proposal, the Bundesrat added a few requests for amendments, including:

- Expanding the group of potential auditors for sustainability reports to include independent assurance providers (in addition to audit firms), and

- Exempting subsidiaries from reporting obligations if a consolidated group report already exists.

By contrast, a proposal by the Economic Affairs Committee to introduce a temporary suspension or reduction of sanctions did not receive majority support. The Bundesrat also expressed its support for a swift EU-level agreement, so that the planned simplifications can still be incorporated into the German law.

What this means for companies in Germany for the 2025 financial year:

- For Wave 1 companies: It is highly likely that the German Bundestag will wait for the final EU Omnibus decision. As a result, Wave 1 companies would continue reporting under NFRD + EU Taxonomy for another year. However, there remains a residual risk that the CSRD implementation law could still be passed before Christmas.Our recommendation:

- ≤1,000 employees → prepare according to NFRD + EU Taxonomy, for example based on the VSME framework

- 1,000 employees → prepare according to ESRS + EU Taxonomy

- For Wave 2–4 companies: Regardless of the national decision, Wave 2–4 companies can expect to begin reporting no earlier than the 2027 financial year. To already benefit from sustainability reporting — for instance, as part of EcoVadis questionnaires or for stakeholders such as customers and banks - without overburdening internal resources, we recommend preparing a VSME report for 2025. Should your company fall under the ESRS reporting obligation starting from the 2027 financial year, the data points can easily be transferred at that time.

For Germany, there are two options:

.avif)

.avif)

.jpg)